Financial

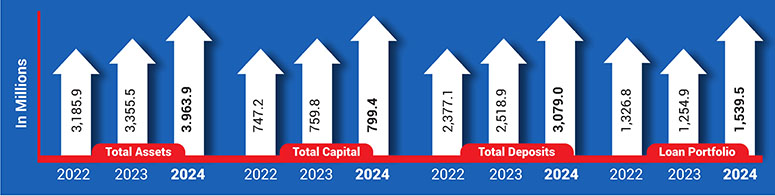

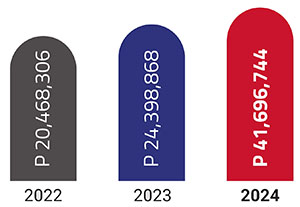

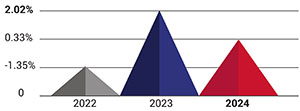

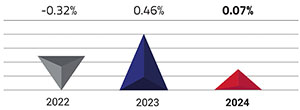

Queenbank maintains a strong balance sheet, and we continue to grow and optimize our deposit and loan portfolio.

Queenbank provides financial services to individuals, corporations, and small and medium entrepreneurs. We

offer a wide range of traditional products and services such as retail banking, consumption, agriculture, auto,

housing, multi-purpose loan, and others.

Network of Branches and ATMs

Queenbank has a reliable and expanding network of delivering its product and services.

Human Resource

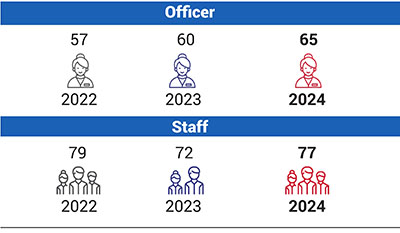

Queenbank is manned by capable and qualified employees having a total workforce of 142 as of the year ended December 31, 2024. Queenbank invests in our employees by providing regular training to foster their knowledge No. of ATMs and career advancement.

Mobile Banking

Queenbank’s mobile banking app has

transformed the way clients access the

bank’s services. With 24/7 availability,

customers can conveniently transfer

funds between Queenbank and other

banks, view real-time exchange rates,

generate personal QR codes, and link

their accounts to e-Wallets. To start

using the app, clients can enroll their

accounts at their mother branch and

receive assistance from Queenbank’s customer service

associates.

The bank’s dedicated team of IT experts is available

24/7 to address any concerns or technical issues that

may arise, further bolstering the safety and reliability of

the mobile banking experience.

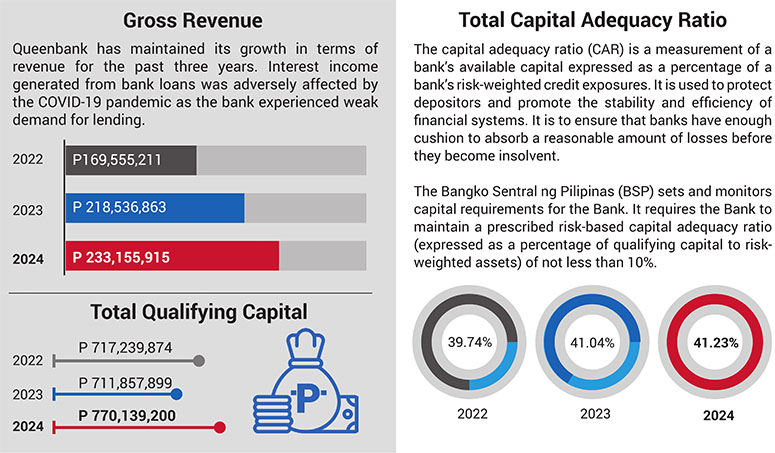

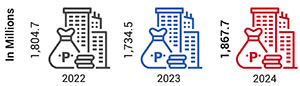

Transferring its Time Deposit placements with private universal banks to Government Securities is a strategic move by the bank to reduce its risk-weighted assets thereby improving its Capital to Risk Asset Ratio (CAR). While the BSP requires all banks to have a minimum of 10% CAR, Queenbank continues to boast a hefty 41.23% CAR as of December 31, 2024.

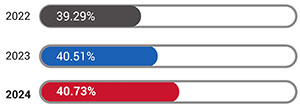

Tier 1 Capital Adequacy Ratio

Tier 1 capital is a bank’s core capital and includes disclosed reserves—that appear on the bank’s financial statements—and equity capital. This money is the funds a bank uses to function regularly and forms the basis of a financial institution’s strength.

Risk-weighted Assets

Risk-weighted assets are used to determine the minimum amount of capital that must be held by banks and other financial institutions to reduce the risk of insolvency. The capital requirement is based on a risk assessment for each type of bank asset.

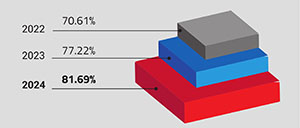

Minimum Liquidity Ratio

Minimum requirement – A prudential MLR of twenty percent (20%) to banks on an ongoing basis absent a period of financial stress. The liquidity ratio is expressed as a percentage that the bank has ability to maintain an adequate level of readily available, high-quality liquid assets that can quickly and easily be converted into cash to meet any liquidity needs that might arise.

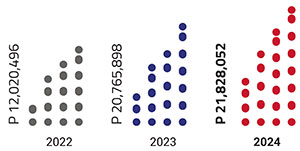

Total Net Interest Income

Refers to the overall profit that Queenbank generates from its interest-bearing activities. It is essentially the difference between the interest income earned on loans and investments and the interest expense paid out to depositors and other lenders.

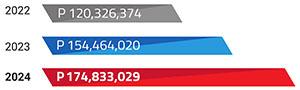

Pre-provision Profit

Pre-provision Profit (PPP) refers to Queenbank’s profit before accounting for funds set aside to cover potential loan losses. It represents the bank’s gross income from its core business activities, excluding the estimated cost of defaults on loans and other credit instruments.

Liquid Assets

Liquid Assets refer to readily available financial assets that can be quickly converted into cash with minimal loss in value. These assets are crucial for banks to maintain their day-to-day operations and meet various financial obligations.

Allowance for Credit Losses

The Allowance for Credit Losses (ACL) is an account that Queenbank maintains to estimate and prepare for potential losses from loan defaults. It’s essentially a financial cushion set aside to absorb situations where borrowers fail to repay their loans in full.

Return on Equity

Return on Equity (ROE) is a key metric that measures the profitability of Queenbank relative to the shareholders’ equity. It essentially indicates how effectively the bank is using its shareholders’ investment to generate profits.

Return on Assets

Return on Assets (ROA) is a profitability metric that measures how efficiently Queenbank utilizes its total assets to generate profit.

Please refer to the attached file.

Queenbank Financial Statements December 31, 2023 and 2024

Please refer to the attached file.

Queenbank's List of Acquired Assets for Sale

Please refer to the attached file.

Published Balance Sheet as of March 31, 2026

Published Balance Sheet as of June 30, 2025

Published Balance Sheet as of March 31, 2025

Published Balance Sheet as of December 31, 2024

Published Balance Sheet as of June 30, 2024

Published Balance Sheet as of March 31, 2024

Published Balance Sheet as of December 31, 2023

-

HEAD OFFICE

Address:

Queenbank Financial Center

Sky City Tower, Mapa Street, Iloilo CityContact Number:

PLDT (033) 336.8052-56

GLOBE (033) 509.8055 loc 1017Email:

customer_service@queenbank.com.ph24/7 Customer Service Hotline:

(033) 501.2403 -

QUEENBANK AFFILIATES

-

ACCREDITATIONS

-

QUEENBANK MOBILE APP

Download Now!

Follow Us