Risks are inherent in all business activities of a bank. Queenbank has adopted a Risk Management System in which it employed processes including identifying, measuring, monitoring, and controlling risk as part of daily activities. We assure that every Queenbanker is responsible for the implementation of our risk management system in order to promote stability and efficiency while risks are mitigated and the realization of opportunities is maximized. The Board of Directors, which sets the tone, has appointed and authorized the Risk Oversight Committee in fulfilling its responsibility in ensuring that the bank is adhering to its risk appetite statement, risk policy, and risk limits as well as its oversight function on the proper implementation of policies and procedures relating to the management of risks. It has three lines of defense in performing the risk management function.

The first line of defense is composed of personnel performing functions related to the delivery of the bank’s products and services, activities designed to generate revenue or reduce expenses, and assistance extended by those under information technology (IT) function to different branches or departments. They belong to front-line units that own and manage the risks and are responsible for implementing corrective actions to address process and control deficiencies.

The second line of defense is performed independently by the Credit Risk Officer and the Compliance function who directly report to the Risk Oversight Committee that helps build and monitor the first line of defense controls. The Credit Risk Officer has the primary function of protecting the bank from credit losses while the Compliance function is an independent function that identifies, assesses, advises on, monitors, and reports on the bank’s compliance risk, that is, the risk of legal or regulatory sanctions, financial loss, or loss to reputation a bank may suffer as a result of its failure to comply with all applicable laws, regulations, codes of conduct and standards of good practice.

The Internal Audit Group serves as the third line of defense considered independent from front-line units, compliance, and other control functions reporting directly to the Audit Committee. They conduct independent assessment and validation through testing of key processes and controls across the company.

The Bank’s Board of Directors has set a risk appetite framework which is reviewed and approved on an annual basis. It provides parameters and guidelines expressed in both qualitative and quantitative terms on the extent to which the bank is willing to put at risk to achieve its strategic objectives and business plans. The bank ensures that exposure to various business activities is within acceptable limits and existing regulatory guidelines. The Bank stands on the following principles:

- Taking risks in a responsible manner that serves the bank’s stakeholders. It is embedded in the bank’s culture that we have a shared responsibility in managing risks and we always strive to maintain an ownership mindset and escalate issues that can be addressed proactively.

- To maintain a strong financial position and be able to generate earnings that are commensurate to the risks taken.

- Assumption of risks based on the Bank’s overall risk capacity and when is capable to identify, measure, monitor, and control the risks.

The Bank has defined credit risk as the risk of loss that the bank faces the situation when the counterparty fails to fulfill wholly or partly of its obligations in a timely manner by breaching contractual obligations or its ability to perform such obligation is impaired resulting in economic loss to the institution. In order to mitigate this risk, our Portfolio Administration Unit follows the credit policy guidelines as provided by the Board. These serve as minimum standards in extending loans to our clientele. Maintenance and strict implementation of sound credit in the granting of loans is observed. We also integrate adequate internal control procedures in the credit—granting process.

Credit risk is controlled through the establishment of appropriate and sufficiently defined environments. We manage this based on the type, economic sector, geographic allocation, maturity, and anticipated profitability of individuals and other borrowers.

In 2015, the Bank initiated the amendments of some of its policies and procedures to conform with BSP Circular No. 855, Guidelines on Sound Credit Risk Management Practices, which include Credit Risk Management Structure and Credit Approval Limits and Delegations. It has likewise updated its product manual on Salary-Based General Purpose Consumption Loans to comply with BSP’s mandate under Circular No. 886.

Stress testing on credit risk is regularly conducted by the Bank which includes Real Estate Stress Test (REST) Limit for Real Estate Exposures and a uniform credit risk stress test on its loan portfolio covering large exposures, exposure to economic activity, and consumer loan.

Market risk arises from adverse movements in the level or volatility of market prices and interest rates of loans, deposits, bonds, investments, and foreign currencies. At Queenbank, the Treasury Group reports to ALCO on the developments and suggests strategies to be adopted.

Operational risk is the current and prospective risk to earnings and capital arising from inadequate or failed internal processes, people, and systems or from external events. The Bank is guided by its Operations Manual, which serves as a policy guideline and makes sure that these are adhered to, properly implemented, and strictly followed. It maintains a close watch over the financial and economic market and oversees operations with care.

The bank’s Internal Audit Group (IAG) monitors strict compliance with these guidelines. It also recommends policies for adoption or for further improvement to the Audit Committee. The Internal Audit Group presents findings and recommendations to the Audit Committee/Board regularly on a monthly basis.

The bank’s Assets and Liability Committee (ALCO) is tasked with monitoring and measuring interest rate risk by identifying gaps between repricing dates of assets and liabilities and minimizing mismatches by accrediting itself to various financial institutions for funding purposes such as BSP rediscounting program, Small and Medium Enterprise Credit (SMEC), and the Small Business Corporation.

The liquidity risk is controlled by the consistent maintenance of well—calculated reserves, accurate measurement and management of funding requirements, effective management of the bank’s access to the financial market, and establishment of updated contingency plans based on the bank’s familiarity with various assumptions underlying the possible cash flows.

This is controlled through the implementation of adequate maintenance procedures for all bank equipment, continuous research and study on the development of systems, and the integration of efficient and highly dependable audit trails in all the bank’s operational systems.

At Queenbank, the Risk Management Committee addresses legal issues that the bank faces. It performs the legal review process for major transactions that the bank may undertake. This committee meets regularly on a monthly basis.

The bank ensures its compliance with laws, rules and regulations, policies and procedures, and ethical standards.

To address this, the bank maintains consistent and adequate compliance with the bank’s operations, proper and timely disclosure of the bank’s condition, and provision of constant information and assurance to the public on the bank’s growth and development plans.

MONEY LAUNDERING AND TERRORIST FINANCING PREVENTION

The bank’s money laundering and terrorist financing prevention program (MTPP) embodies sound risk management policies and practices that have been developed to ensure that risks associated with money laundering, terrorist financing, and proliferation financing are identified, assessed, monitored, mitigated and controlled and to make certain that by effectively implementing it, the bank shall not be used as a vehicle to legitimize proceeds of unlawful activity or to facilitate or finance terrorism.

The MTPP is geared toward the promotion of high ethical and professional standards and the prevention of the bank being intentionally or unintentionally used for money laundering and terrorism financing. The program consists of thorough customer due diligence and know-your-customer processes, targeted financial sanctions, reporting of Covered and Suspicious Transactions, and retention of records. It likewise includes effective and continuous training programs including refresher training to promote full awareness and thorough understanding of officers and employees of their respective duties and responsibilities and that they carry them out in accordance with superior and principled culture of compliance. A mandate is provided that the bank shall adequately screen job applicants according to the standards set forth in the Human Resource Policy Manual to ensure only qualified personnel without criminal records are employed to assume sensitive banking functions.

The bank is regularly reviewing the program in order to incorporate updates needed to be brought by legislative and regulatory developments. The Compliance Group and the Risk Oversight Committee are responsible of this function. The Board of Directors and management propel all employees to conduct business in conformity with high ethical standards in order to protect the safety and soundness as well as the integrity of the bank and the national banking and financial system.

EMPLOYEE WELFARE

The Bank values the performance and contribution of employees. It believes that performance review is a key component of employee development. An annual review through a performance appraisal sheet is utilized by the officers to properly be guided on how to evaluate their designated staff. It is required and designed to provide a fair assessment of an employee’s job performance (outcomes and behavior). The immediate supervisor should discuss with the employee his/her performance during the previous calendar year, job duties, performance expectations, any specific objectives to be achieved, and professional development goals for the employee.

The Bank’s board-level committees such as the Audit Committee, Risk Oversight Committee and Related Party Committee, management committee that includes ALCO, Executive Committee and Credit Committee, and selfassessment functions comprising of Internal Audit Group and Compliance Group are evaluated annually. In addition, the Chairman/President and Senior Officers are evaluated by the Board of Directors on a yearly basis. To properly assess one’s performance, the Bank is also conducting a Board Self-Assessment to validate the board’s appreciation of its roles and responsibilities.

Education and training programs are designed, in accordance with the Bank’s objectives and strategies, to meet the personal and career development needs of all employees. Orientation is part of a long-term investment in a new employee. It is an initial process that provides easy access to basic information and gives clarification and allows new employees to take an active role in the Bank. The process of which includes the introduction of new employees to its new environment, informing about company policies and procedures, and discussion and understanding of the Bank’s Code of Discipline. This is for the purpose of setting an expectation as to how employees should conduct as a Queenbanker. The bank secures training programs and seminars for the members of the Senior Management as to keep them abreast of the updates and changes in the banking sector.

It is a requisite for the members of the Board of Directors to attend the continuing Corporate Governance training to ensure that they continuously possess the knowledge required for their positions. It covers areas on how to adapt to changes in Corporate Governance Code and Internal Control Environment, Enterprise Risk Management, and Fraud Awareness. In addition, they are equipped with the latest rules and regulations issued by the SEC and BSP.

Queenbank plans for its manpower needs as far ahead as possible. Thus, the bank endeavors to maintain a required number of employees, possessing the necessary skills, experience, and qualifications, to efficiently carry out its operations. It has a documented succession plan to cover the eventuality of an individual holding a key position that can no longer be employed by the bank.

Line management, in conjunction with Human Resource Group, identifies individuals demonstrating superior performance and potential for future promotion. These individuals will then be assessed for the training and development they further need in order to prepare them to a higher level whenever it becomes vacant.

For the retirement age of directors, the bank gives importance to the expertise and experiences of the senior director and the valuable wisdom he or she can impart to the Board. It also acknowledges that age is not the main factor in determining the effectiveness of the director in discharging its duties and responsibilities. The bank has no existing retirement age policy for directors as long as they comply with the fit and proper requirements of the bank. As for Independent Directors, they may serve for a maximum cumulative term of nine years after which, he or she shall be perpetually barred from serving as such, but may continue to qualify for election as a regular Director.

For the succession or any vacancies in the Board of Directors, it shall be filled by a majority vote of the members of the Board of Directors constituting a quorum at a meeting specially called for that purpose.

The bank’s retirement and succession plan is reviewed annually. Any changes or updates are to be concurred by the Head of the Human Resource Group and the Executive Committee.

Remuneration Policy and Structure for Executive and Non-Executive Directors and Senior Management

The Bank’s remuneration policy is aligned with the Bank’s overall strategic plan, objectives, and values. The Bank from time to time, as determined by an annual/periodic review thereof, may adjust the salary as appropriate, taking into account the Bank’s performance, the employee’s performance, and the prevailing economic conditions.

The remuneration of Executive Directors consists of a fixed salary, director’s fee, and pension benefits. They are also entitled to fringe benefits such as car subsidies, medical insurance, and other fixed benefits. Non-Executive Directors, on the other hand, receive allowances and per diems for each attendance at board meetings or board-level committee meetings. Senior Management receives allowances and fixed salary which is determined on the basis of the nature of the position, including responsibility and its complexity. Remuneration to Directors and Senior Management is reviewed annually and approved by the Board.

Dividends policy states that the cash dividends to be declared to shareholders should be in accordance with the BSP and SEC rules on declaration and requires the approval of the majority of the Board of Directors. Once approved, necessary disclosures are made in compliance with regulatory requirements.

Transactions such as loans, lease agreements/contracts, and

purchases and sales of assets to related parties (stockholders,

directors, senior officers, related interest and subsidiaries) are

evaluated by the Related Party Committee to ensure that these

are undertaken on an arm’s length transaction and not on a

more favorable economic terms than similar transactions with

non-related parties.

The management implements appropriate controls to

effectively manage and monitor related party transactions on a

per-transaction and aggregate basis. Ongoing monitoring of the

exposures to related parties is conducted to ensure compliance

with the policy and BSP’s regulations thru the internal audit and

compliance function.

Transactions with related parties and with DOSRI are discussed

in Note 26 of the Audited Financial Statements.

The bank’s Internal Audit Group provides an independent, objective assurance and consulting activity designed to examine, evaluate and improve the effectiveness of risk management, internal control, governance processes, and compliance thereby adding value and enhancing the quality of the bank’s operations. The group consists of an Internal Audit Head and audit staff who have undergone continuous education on auditing techniques, regulations, and banking products and services. The internal audit head reports directly to the board of directors through the Audit Committee which ensures that the group is independent from the bank’s management.

The Compliance Unit is an independent unit that oversees and coordinates the implementation of the compliance program, identifies the relevant Philippine laws and regulations, analyzes the corresponding risks of non-compliance and identifies, monitors, and controls these risks. The Chief Compliance Officer is free to report to Senior Management and to the Board of Directors thru the Risk Oversight Committee on any irregularities or breaches of laws, rules, and standards discovered, without fear of retaliation or disfavor from the management or other affected parties.

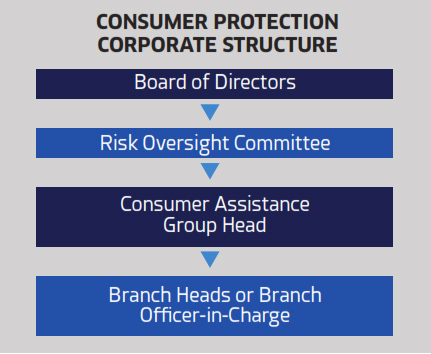

The Board of Directors (BOD) has the ultimate responsibility for

the level of customer risk assumed by Queenbank. Accordingly,

the Board approves the Bank’s overall business strategies

and significant policies, including those related to managing

and taking customer risks. They take steps to develop an

appropriate understanding of the customer risks the Bank

faces through briefings from auditors and experts external

to the organization. Senior management is responsible for

implementing a program to manage the customer compliance

risks associated with the Bank’s business model and ensuring

compliance with laws and regulations on both a long-term and

a day-to-day basis. Accordingly, management is fully involved

in its activities and possesses sufficient knowledge of all

major products to ensure that appropriate risk controls are in

place and that accountability and lines of authority are clearly

delineated. They are also responsible for establishing and

communicating a strong awareness of, and need for, effective

customer protection risk controls and high ethical standards.

Queenbank acknowledges the indispensable role of its

financial consumers in bringing about a strong and stable

financial system, their right to be protected in all stages of their

transactions with the bank, and be given an avenue to air their

grievances in the product and services of the bank. Consumer

protection is regarded as a core function complementary to

BSP’s prudential regulation and supervision, financial stability,

financial inclusion, and financial education agenda.

Queenbank’s Consumer Assistance Group is composed of the Consumer Assistance Group Head which is handled by the bank’s Compliance Officer and Branch Heads or Branch Officer-In-Charge of every Queenbank branch are designated to handle consumer concerns.

-

HEAD OFFICE

Address:

Queenbank Financial Center

Sky City Tower, Mapa Street, Iloilo CityContact Number:

PLDT (033) 336.8052-56

GLOBE (033) 509.8055 loc 1017Email:

customer_service@queenbank.com.ph24/7 Customer Service Hotline:

(033) 501.2403 -

QUEENBANK AFFILIATES

-

ACCREDITATIONS

-

QUEENBANK MOBILE APP

Download Now!

Follow Us